The Shifting Landscape: Netflix's Evolving Share in the Streaming Originals Top Ten

In the dynamic world of streaming entertainment, narratives often swing between extremes. One moment, a single platform is declared the undisputed champion; the next, its imminent demise is predicted. The "streaming wars" have fueled countless headlines, many leaning towards hyperbole to capture attention. While dramatic pronouncements can drive clicks and shares, a deeper understanding of the market requires a more nuanced, data-driven approach.

Analyzing long-term trends, rather than focusing on isolated weekly fluctuations, provides a clearer picture of the competitive landscape. One particularly insightful metric, tracked by Nielsen, is the composition of the weekly Top Ten Streaming Originals chart in the United States. This chart, based on viewership minutes, offers a glimpse into which platforms are successfully capturing significant audience attention with their new, exclusive programming.

For years, Netflix held a seemingly unshakeable dominance over this list. As the pioneer and market leader, its originals frequently occupied the majority of the top spots, sometimes leaving only a handful for all other competitors combined. This dominance was a reflection of Netflix's massive subscriber base, its prolific content output, and its early mover advantage in establishing viewing habits.

Analyzing the Data: A Clear Trend Emerges

A look at the historical data from Nielsen's Top Ten Streaming Originals chart reveals a significant shift over the past few years. While Netflix still consistently places titles on the list, its *share* of the ten available spots has demonstrably decreased.

Consider the trend over time. In 2021, Netflix originals frequently accounted for 80% or more of the titles appearing in the weekly Top Ten. This meant that in a given week, eight out of the ten most-watched original streaming series or films were typically found on Netflix. This level of dominance underscored the platform's central role in the streaming ecosystem and its ability to consistently produce content that resonated with a broad audience.

However, this picture has changed. By 2024 and into 2025, Netflix's share of the Top Ten Originals has fallen considerably. Data indicates this share has dropped to around 52% on average so far this year. This represents a substantial decline of 28 percentage points from the 2021 baseline. While 52% is still a majority share, it signifies a market where nearly half of the top-performing original titles are now coming from other platforms.

This trend isn't always a smooth, linear descent. Weekly numbers can fluctuate based on major new releases. A blockbuster Netflix show might temporarily push their share higher in a specific week, as seen in the example provided where Netflix held four spots in late March. However, the overall pattern, when viewed across months and years, clearly points towards a more fragmented distribution of top original hits across multiple services.

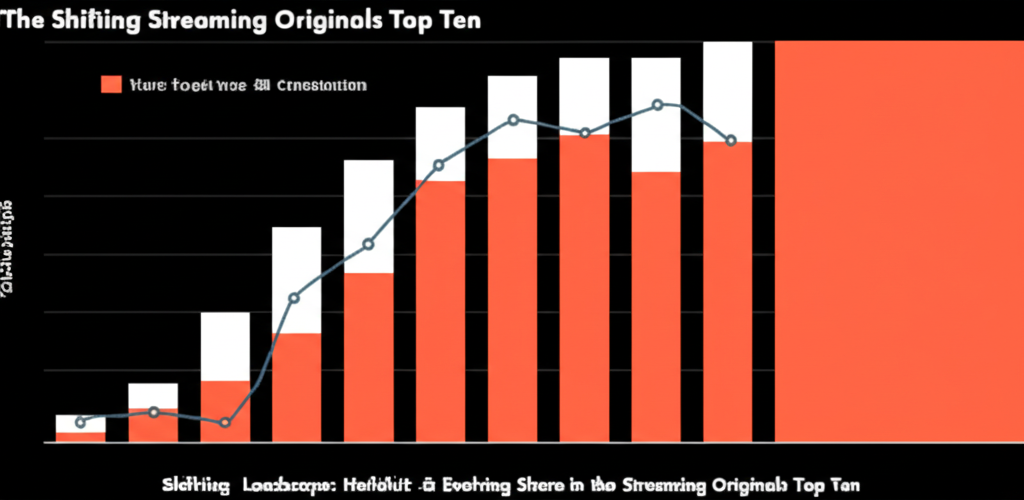

Visualizing the Shift

The data becomes even clearer when visualized over different time intervals:

- Weekly View: A stacked bar chart showing the weekly breakdown of the Top Ten by platform reveals the week-to-week variability but also the gradual erosion of Netflix's consistent high share. While spikes occur, the baseline average declines.

Image: Weekly Share of Nielsen Top 10 Originals Chart (Source: Entertainment Strategy Guy)- Monthly View: Aggregating the data by month smooths out some of the weekly noise, making the downward trend in Netflix's share and the corresponding upward trend for other streamers more apparent.

Image: Monthly Share of Nielsen Top 10 Originals Chart (Source: Entertainment Strategy Guy)- Annual View: The most striking visualization is the annual average share. This clearly shows the percentage decline for Netflix year-over-year since 2021 and the collective gain by other platforms.

Image: Annual Share of Nielsen Top 10 Originals Chart (Source: Entertainment Strategy Guy)

These charts, using data from Nielsen covering the US market from 2021 to the present, measured by the count of titles in the Top Ten Originals weekly list, consistently demonstrate the same core conclusion: the streaming market, at least in terms of top-performing original content, is becoming more competitive.

The Rise of the Challengers

The decline in Netflix's share isn't happening in a vacuum. It's a direct consequence of the significant investments made by other major media companies in their own streaming services and original content libraries. Companies like Disney (Disney+, Hulu), Warner Bros. Discovery (Max), Paramount Global (Paramount+), NBCUniversal (Peacock), and Apple (Apple TV+) have entered or significantly ramped up their presence in the streaming arena over the past few years.

These competitors have leveraged their vast existing intellectual property, deep pockets, and established production capabilities to create original series and films designed to compete directly with Netflix's offerings. Successful originals like those on Disney+ (Marvel and Star Wars series), Max (HBO content and new originals), and Apple TV+ (critically acclaimed dramas and comedies) have increasingly found their way onto Nielsen's Top Ten charts, chipping away at Netflix's former dominance.

The strategy for many of these newer entrants has been to focus on high-profile, often franchise-driven, original content that can quickly capture audience attention and drive subscriptions. While their overall content libraries might be smaller than Netflix's, their ability to land multiple titles in the Top Ten in a given week signals their growing effectiveness in producing popular hits.

Understanding the Nuances and Caveats

As the original author correctly points out, reality is filled with nuance. While the trend in the Nielsen Top Ten Originals chart is a strong indicator of increased competition, it's essential to consider the caveats:

- Focus on Originals: The chart specifically tracks *original* streaming content. It does not include licensed movies or TV shows, which still constitute a significant portion of viewership on many platforms, including Netflix. A platform might have a lower share of original hits but still command high overall viewership due to popular library content.

- Count vs. Viewership Minutes: The analysis focuses on the *count* of titles in the Top Ten. It doesn't differentiate between a show that barely makes the list at number ten and a massive phenomenon that generates significantly more viewing minutes than any other title. Netflix still frequently has the number one show by a large margin, even if it only has a few titles in the rest of the list.

- US Market Only: Nielsen's public Top Ten data primarily covers the US market. The competitive dynamics and popular titles can vary significantly in international markets, where Netflix often retains a stronger lead due to its earlier global expansion.

- Methodology: Nielsen's methodology, while widely cited, has its own limitations and is constantly evolving. Other measurement firms might produce slightly different results.

- Defining "Original": The definition of a "streaming original" can sometimes be complex, especially with content that premieres on a linear network before moving to streaming, or co-productions.

These nuances do not invalidate the core trend of increased competition in the battle for top original hits, but they provide crucial context. Netflix's declining *share* of the Top Ten Originals doesn't necessarily mean its *total* viewership is plummeting or that it's no longer the leading service overall. It means that other services are now consistently producing content popular enough to break into the top ranks, making the competition for audience attention with new shows and movies much fiercer.

Implications for the Streaming Ecosystem

The shift in the Top Ten Originals landscape has several significant implications for the streaming industry:

Increased Content Spending Pressure: To compete for those coveted Top Ten spots, streamers must continue investing heavily in high-quality, marketable original content. This drives up production costs across the industry.

Focus on Hits: The data reinforces the "hit-driven" nature of the entertainment business. While library content provides viewing volume, it's often the buzzy new originals that drive subscriptions and appear on these top lists. This puts pressure on platforms to consistently deliver breakout shows.

Diversification of Content Sources: Consumers now have a wider array of platforms successfully producing popular originals. This reduces reliance on a single service for must-watch new shows and encourages multi-service subscriptions or churn as viewers follow specific titles.

Strategic Shifts: Streamers are adapting their strategies. Some are exploring hybrid release models (theatrical windows before streaming), incorporating advertising tiers to boost revenue, and focusing on specific genres or demographics where they can uniquely compete. The pursuit of profitability is also leading to more scrutiny of content budgets and performance.

Measurement Matters: As the market matures, accurate and comprehensive measurement becomes more critical. Data like Nielsen's Top Ten provides one valuable perspective, but platforms and analysts are increasingly looking at a wider range of metrics, including subscriber engagement, retention, and profitability per title.

The Future of the Streaming Wars

The trend observed in the Nielsen Top Ten Originals chart suggests that the "streaming wars" are far from over; in fact, they are intensifying on the front of original content performance. While Netflix maintains a strong position, it no longer enjoys the near-monopoly on top original hits it once did.

The coming years will likely see continued evolution. Will some platforms merge or consolidate? Will advertising tiers become the norm? How will global expansion strategies impact the US market? These are complex questions with no simple answers, requiring ongoing analysis based on data, not just dramatic headlines.

What is clear from the Nielsen data on Top Ten Originals is that the competitive intensity has increased. Other players have successfully entered the arena and are consistently producing content that captures significant audience attention, challenging Netflix's long-held dominance in this specific, but important, metric. Understanding this shift, with all its nuances, is key to grasping the current state and future direction of the streaming landscape.

External Perspectives on the Streaming Market

Industry analysts and journalists frequently cover the evolving dynamics of the streaming market, offering additional context and perspectives on the trends highlighted by Nielsen data. Reports often delve into the financial performance of streaming companies, subscriber growth (or lack thereof), content strategies, and the impact of advertising tiers.

For instance, articles on TechCrunch often cover the business and technology angles of streaming, including funding, new features, and market shifts. Wired frequently explores the cultural impact of streaming, content trends, and the user experience. VentureBeat provides insights into the media technology sector, including streaming platforms and their strategic moves.

These sources often cite Nielsen data or other measurement firms when discussing viewership trends and market share. They might analyze specific hit shows, discuss the effectiveness of different release strategies, or report on executive commentary regarding the state of the industry. For example, a TechCrunch article might detail how a specific platform's new original series drove app downloads, or a Wired piece could discuss the cultural phenomenon created by a show that topped the Nielsen charts.

Analyzing reports from these credible sources alongside the raw data provides a more comprehensive understanding of the forces shaping the streaming wars. They help connect the dots between data points, strategic decisions by companies, and the broader economic and technological factors at play.

While specific images from these sites would ideally be embedded to illustrate points (e.g., a graph of streaming service growth from VentureBeat, a screenshot related to a major show discussed on Wired, or a photo of a tech executive from TechCrunch), their inclusion would depend on specific licensing and availability. However, the reporting from these outlets consistently reinforces the picture of a market where competition for viewer attention, particularly with original content, is increasingly fierce.

Conclusion: Competition is the New Normal

The data from Nielsen's Top Ten Streaming Originals chart provides compelling evidence that the streaming landscape is becoming significantly more competitive. Netflix's once overwhelming dominance in placing original titles on this key viewership list has diminished, not because Netflix is failing, but because its competitors have successfully elevated their game.

The streaming wars narrative, while sometimes oversimplified, captures a fundamental truth: multiple powerful players are vying for limited consumer time and money. The decline in Netflix's share of top original hits is a tangible manifestation of this competition.

Moving forward, success in streaming will likely depend less on simply having the largest library and more on the ability to consistently produce compelling, high-performing original content that cuts through the clutter, alongside smart business models that ensure profitability in a high-cost environment. The era of one streamer dominating the conversation around original hits is giving way to a more fragmented, competitive future.

Understanding this shift requires looking beyond the headlines and diving into the data, acknowledging the nuances, and recognizing that the battle for streaming supremacy is being fought, and increasingly won, on multiple fronts by a growing number of formidable players.